What is a CD (Certificate of Deposit)

Susan Kelly

Nov 23, 2023

The interest rate on a CD, or certificate of deposit, is fixed and typically greater than the interest rate on a conventional savings account. Additionally, it has a predetermined term end date and a predetermined withdrawal date or maturity date. Investors lock money in a CD for a term typically six months to five years. Although most CDs have an early withdrawal fee or penalty, they do not have monthly fees.

Certificates of Deposit, like conventional savings accounts, are insured, so you'll receive your money back if your bank fails. The Federal Deposit Insurance Corporation (FDIC) insures bank CDs.

How Does a CD Work

Opening a CD account follows the same steps as opening other bank accounts: Apply at a banking institution in person or online. The main difference is that, almost always, your initial investment into a CD will be the only one you can make, not like a conventional savings or checking account, where you can add funds over time.

When a CD's term expires, the interest earned is typically compounded, allocated to your bank account daily or monthly, and paid to you in full. (Or, if the bank permits it, you can decide to get interest payments regularly.)

When the term of a CD expires, a bank will usually renew it at a new interest rate, which is frequently the same as that of new CDs with the same term. Since looking for the best CD rates whenever you open a new CD account is preferable, doing this may not be in your best interests.

CD Vs. Savings Accounts

A certificate of deposit (CD) is a unique form of savings tool. Like a savings account, CDs offer an opportunity to save funds you don't necessarily need for day-to-day spending while receiving a particular return on your balance. Examples of savings goals include saving for a down payment on a home, a new car, or a big trip.

One initial CD deposit must stay in the bank account until the CD matures, six or five years from now. CDs typically provide higher rates of return than savings accounts in exchange for handing away access to your money.

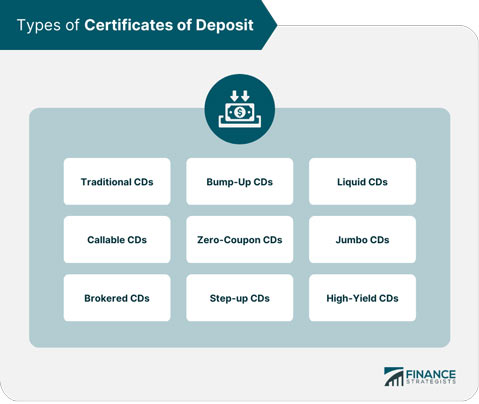

Types of CDs

Common features of a CD include a fixed rate of return and a fixed term. However, depending on your bank, you might have access to a few other options.

No-penalty or Liquid CD: The liquid CD enables the depositor to withdraw money anytime during the term without penalty or fees. Liquid CDs offer lower interest rates than fixed-term regular CDs.

Bump-up CD: With this type, you can boost the interest rate if it rises after you purchase a CD. The Bump-up CD offers lower interest rates than the Standard CD. You must wait for a bank rate increase to receive more earnings. You'd be stuck paying the initial rate if the rates weren't raised.

Step-up CD: A step-up CD works much like a bump-up CD. Even yet, the bank initiates the gradual interest rate increases on its own.

High-yield CD: This type of CD offers higher rates than average. Interest rates at conventional banking institutions are often higher than those at online banks or credit unions.

Broker CD: This type of CD is provided by a third party or broker, such as a brokerage company.

Jumbo CD: This type comes with a high minimum balance requirement (often $100,000) in exchange for customarily higher interest rates.

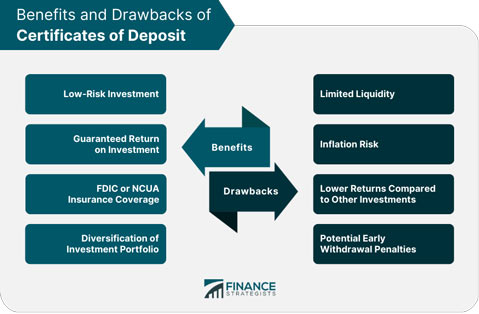

Advantages and Disadvantages of CDs

Let's explore the benefits and drawbacks of certificates of deposit (CD).

Advantages of CD

- CDs have lower risks than other financial instruments like equities, bonds, etc. Since they are held with banks, they are less susceptible to market fluctuations than stocks are. Many also have access to federal insurance.

- Some online financial institutions and banks offer very high-yielding products that investors can investigate to generate greater returns.

- CDs offer higher returns for the amount invested than the standard savings account.

- A depositor can reinvest their money once a CD reaches maturity using rollover choices into a new CD.

Disadvantages of CD

- Certificates of deposits are not liquid assets because the money has been frozen for a specific time. A withdrawal penalty is usually associated with deposit withdrawals made before expiration.

- Low-risk investments have extremely low returns compared to equities, stocks, or bonds.

- Fixed interest rates can cost if rates increase during the CD term

Bottom Line

For those who want to increase their returns without taking on the risk associated with stocks and bonds, certificates of deposit (CD) offer stability. Although locking up your money for a long period may be safe, if the Fed funds rate rises, you might miss out on higher returns. Although you can take your money out beforehand, there will be fees associated with it, some of which may reduce your principal. Before you sign the contract, be aware of the advantages and restrictions of your potential investment.